Trusted Worldwide Questions & Answers

APA FPC-Remote Dumps - Pass the Fundamental Payroll Certification Exam in First Attempt 2026

The APA FPC-Remote - Fundamental Payroll Certification Exam is designed for candidates pursuing the Fundamental Payroll certification and validating their payroll knowledge. It is a strong choice for professionals who want to demonstrate practical understanding of payroll concepts, compliance, administration, and calculations. This exam matters because it confirms that you can apply payroll knowledge accurately in real workplace situations. Preparing well for FPC-Remote helps you build confidence and improve your chances of success on exam day.

Exam Topics Overview

| # | Exam Topics | Sub-Topics | Approximate Weightage (%) |

|---|---|---|---|

| 1 | Core Payroll Concepts | Payroll terminology, pay cycles, gross-to-net basics, employee classifications | 18% |

| 2 | Compliance / Research and Resources | Payroll laws, research methods, reference tools, compliance updates | 16% |

| 3 | Calculation of the Paycheck | Wages and deductions, overtime, taxes, net pay, paycheck calculations | 20% |

| 4 | Payroll Process and Supporting Systems and Administration | Payroll workflow, system inputs, employee data, processing controls | 14% |

| 5 | Payroll Administration and Management | Policies and procedures, record handling, team coordination, payroll governance | 12% |

| 6 | Audits | Audit preparation, error detection, reconciliation, reporting checks | 10% |

| 7 | Accounting | Payroll journal entries, liabilities, balancing, accounting controls | 10% |

This exam tests more than memorization. Candidates must understand payroll processes, apply calculations correctly, recognize compliance requirements, and interpret payroll-related records with practical accuracy. Strong attention to detail, sound judgment, and familiarity with payroll administration are important for success.

How QA4Exam.com Helps You Pass

QA4Exam.com offers an Exam PDF with actual questions and answers plus an Online Practice Test to help you prepare for the APA FPC-Remote exam efficiently. The practice materials are built to simulate the real exam experience, so you can get comfortable with question style, pacing, and time management. With up-to-date questions and verified answers, you can review important topics with more confidence and focus on what matters most. Using both the PDF and the online test gives you a practical way to strengthen weak areas and improve your readiness for passing the exam on your first attempt.

Frequently Asked Questions

The questions for FPC-Remote were last updated on Jul 18, 2026.

- Viewing page 1 out of 32 pages.

- Viewing questions 1-5 out of 162 questions

Examples of active listening include all of the following actions EXCEPT:

Comprehensive and Detailed Explanation:

Active listening is an essential payroll communication skill that ensures employees receive accurate information.

Option A (Affirming verbally) Shows understanding and engagement.

Option C (Paraphrasing the discussion) Ensures clarity and accuracy.

Option D (Asking open-ended questions) Encourages better dialogue.

Option B (Interjecting an opinion) is incorrect because it can disrupt communication and cause misunderstandings.

Payroll.org -- Customer Service and Communication Best Practices

HR Compliance Training -- Effective Workplace Communication

The journal is commonly referred to as the record of:

A journal is known as the 'original entry' because transactions are first recorded here before posting to the ledger.

The general ledger is the final entry (B), not the journal.

Payroll Accounting Standards (Payroll.org)

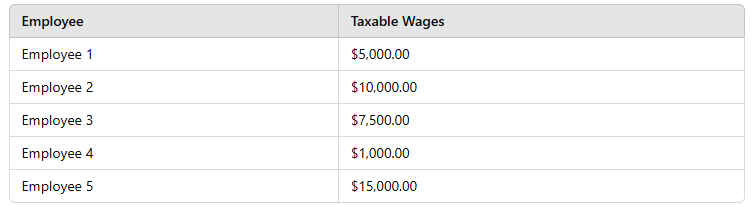

Using the table of taxable wages below, calculate the employer's FICA tax liability on the first check of the year:

Total Taxable Wages:

$5,000 + $10,000 + $7,500 + $1,000 + $15,000 = $38,500

Social Security Tax (6.2%)

$38,500 6.2% = $2,387.00

Medicare Tax (1.45%)

$38,500 1.45% = $558.25

Total FICA Tax (Employer's share)

$2,387.00 + $558.25 = $2,945.25

IRS Publication 15 (Employer's Tax Guide)

A payroll employee has just entered a group of timecards for one of their 25 retail stores. What is the BEST way to verify that the data was entered accurately?

Comprehensive and Detailed Explanation:

The best way to verify payroll accuracy is to run a batch total report (Option D) because it:

Compares actual payroll totals to expected amounts

Identifies discrepancies before payroll processing

Option A (Review a few employees) is insufficient because errors in other records might be missed.

Option B (Check Register) occurs after payroll is processed.

Option C (Earnings Report) is useful but is generated after payroll is processed, making corrections harder.

Payroll.org -- Payroll Data Verification Best Practices

IRS -- Payroll Accuracy and Compliance Guidelines

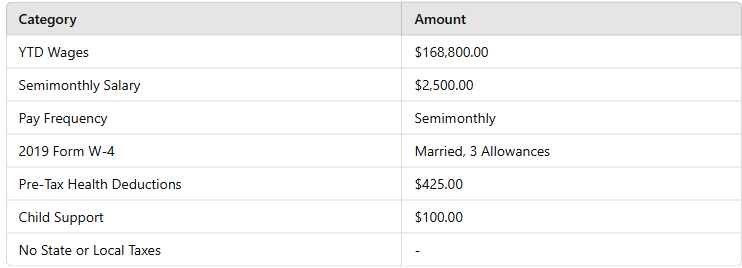

Based on the following information, using the percentage method, calculate the employee's net pay:

Comprehensive and Detailed Explanation:

Using the IRS Percentage Method for Married Filing Jointly (2019 W-4):

Calculate taxable wages:

Gross pay: $2,500.00

Less pre-tax deductions: -$425.00

Taxable wages: $2,075.00

Federal Income Tax (from IRS tax tables):

Using 2019 IRS Percentage Method for Married, Semimonthly Pay:

First $1,640.00 taxed at 10% = $164.00

Remaining $435.00 taxed at 12% = $52.20

Total FIT = $216.20

Social Security Tax (6.2%):

$2,500.00 6.2% = $155.00

Medicare Tax (1.45%):

$2,500.00 1.45% = $36.25

Other deductions:

Child Support: $100.00

Total Taxes and Deductions:

216.20+155.00+36.25+100.00=507.45216.20 + 155.00 + 36.25 + 100.00 = 507.45216.20+155.00+36.25+100.00=507.45

Net Pay Calculation:

2,500.00507.45=1,730.362,500.00 - 507.45 = 1,730.362,500.00507.45=1,730.36

Thus, the correct answer is B. $1,730.36.

IRS Publication 15-T -- Federal Income Tax Withholding Methods

Payroll.org -- Net Pay Calculation Guide

Unlock All Questions for APA FPC-Remote Exam

Full Exam Access, Actual Exam Questions, Validated Answers, Anytime Anywhere, No Download Limits, No Practice Limits

Get All 162 Questions & Answers