Trusted Worldwide Questions & Answers

CFA Institute CFA-Level-II Dumps - Pass CFA Level II Chartered Financial Analyst Exam in 2026

The CFA Institute CFA-Level-II - CFA Level II Chartered Financial Analyst exam is a key step in the CFA Level II certification path. It is designed for candidates who want to deepen their ability to analyze complex financial data and apply investment concepts in realistic scenarios. This exam matters because it demonstrates advanced knowledge that is valued by employers across the investment and finance industry. Preparing well for it can help candidates move closer to earning the CFA Level II credential.

| # | Exam Topics | Sub-Topics | Approximate Weightage (%) |

|---|---|---|---|

| 1 | Ethical and Professional Standards | Code and Standards application, ethical decision-making, professional conduct, conflicts of interest | 10% |

| 2 | Quantitative Methods | Statistical concepts, regression analysis, time-series analysis, model interpretation | 8% |

| 3 | Economics | Market structure, macroeconomic analysis, currency exchange concepts, economic indicators | 8% |

| 4 | Financial Statement Analysis | Income statement analysis, balance sheet analysis, cash flow analysis, intercorporate investments | 12% |

| 5 | Corporate Issuers | Corporate governance, capital budgeting, cost of capital, working capital management | 8% |

| 6 | Equity Investments | Industry analysis, valuation concepts, market organization, equity portfolio management | 14% |

| 7 | Fixed Income | Bond pricing, yield measures, term structure, credit analysis | 14% |

| 8 | Derivatives | Forward contracts, futures, options, swap valuation basics | 8% |

| 9 | Alternative Investments | Real estate, private equity, commodities, hedge fund strategies | 7% |

| 10 | Portfolio Management and Wealth Planning | Portfolio risk and return, asset allocation, investor objectives, wealth planning concepts | 11% |

The exam tests more than memorization. Candidates must show strong analytical skills, a clear understanding of investment concepts, and the ability to apply knowledge to case-based questions. It also measures judgment, precision, and the capacity to work through complex scenarios under time pressure.

How QA4Exam.com Helps You Pass

QA4Exam.com offers an Exam PDF with actual questions and answers plus an Online Practice Test that helps you prepare in a focused way for CFA Institute CFA-Level-II. The materials are designed to give you a real exam simulation so you can get comfortable with the format and pacing before test day. With up-to-date questions and verified answers, you can study with more confidence and reduce last-minute uncertainty. The practice test also helps you improve time management, spot weak areas, and build the speed needed to finish the exam efficiently. If your goal is to pass on the first attempt, these resources can support a more targeted and practical preparation plan.

FAQ

It is for candidates pursuing the CFA Level II certification path who want to build deeper investment analysis skills and advance their finance knowledge.

Yes, it is generally considered challenging because it tests analytical thinking, topic integration, and the ability to apply concepts in detailed scenarios.

Braindumps alone are not a complete preparation strategy. They can help you review question patterns and reinforce concepts, but you should also study the exam topics and practice applying them.

Hands-on experience can help you understand the material more naturally, but the exam preparation itself is focused on knowledge, analysis, and application rather than job experience alone.

QA4Exam.com dumps and the Online Practice Test are helpful tools for review and exam simulation, but combining them with topic study can improve your readiness and confidence.

Yes, they are designed to help you prepare efficiently with verified answers, realistic practice, and time management training, which can improve your chances of passing on the first attempt.

The Exam PDF provides actual questions and answers for review, while the Online Practice Test gives you a simulated test experience to practice under exam-like conditions.

The questions for CFA-Level-II were last updated on Jul 20, 2026.

- Viewing page 1 out of 143 pages.

- Viewing questions 1-5 out of 715 questions

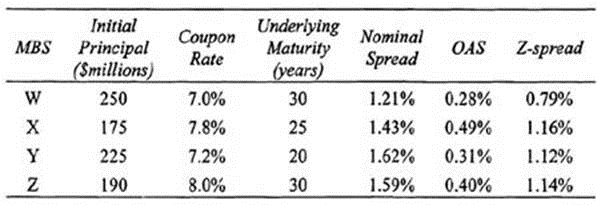

Christopher Robinson, chairman of the board of directors for a private endowment fund, believes that the endowment fund for which he is responsible has diverged too far from its stated objectives. Over several years the board has increased the size of the fund's equity position beyond the stated limits of the investment policy statement. In an effort to realign the fund's investments, Robinson has elected to choose a mortgage-backed security (MBS) for inclusion in the endowment's portfolio. After surveying the MBS market, Robinson has selected four MBS securities to present as potential investments at the next investment committee meeting. Details on the selected MBS securities are presented below:

At the investment committee meeting, a fellow board member raises his concerns over the potential MBS investments stating, "While we all agree that the fixed-income proportion of the endowment is much too small, I am not sure the suggested MBS securities will fulfill the cash flow requirements of the endowment. What risks are we taking on by allocating a portion of the portfolio to these investments? We cannot afford to end up with a timing mismatch between the cash needs of the endowment and the cash provided from its investments. Also, we have given no consideration to commercial mortgage backed securities (CMBS). Isn't our analysis incomplete if we fail to give proper discussion of potential CMBS investment opportunities?"

Robinson responded to his fellow board member by addressing the board member's concerns as follows:

"Since the cash requirements of the endowment fund fluctuate directly with interest rates, the cash flows provided from the MBS will provide adequate protection against cash shortfalls arising from differences in the timing of cash needs and cash sources. In addition, we can further reduce uncertainty surrounding the timing of cash flows by purchasing planned amortization class CMOs, which are securities issued against pools of MBS. CMBS were not presented due to the unacceptable risk profile of the comparable CMBS trading in the marketplace."

Determine the single month mortality rate for MBS-X for Month 20 using 200 PSA .

First find the appropriate CPR by using the following formula: 6%X . In this problem t will equal 20 since this is the month of interest.

The CPRs using 200 PSA is: 6% x x 2.00 = 8.0%.

Then, use the following equation to find the SMM: SMM = 1 - (l---CPR .

The SMM for 200 PSA is: and = 1 -(l -0.08 = 0.0069.

(Study Session l5,LOS 55.c)

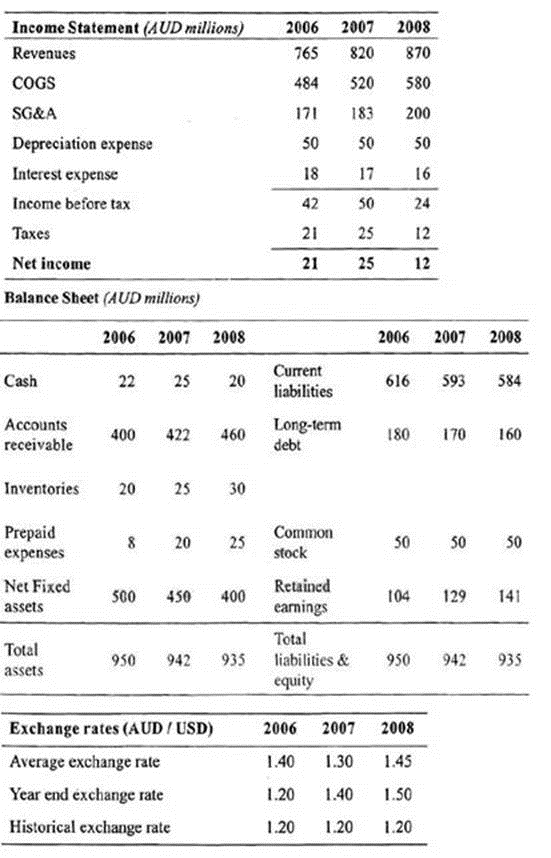

Gary Smith, CFA, has been hired lo analyze a specialty tool and machinery manufacturer, Whitmore Corporation (WMC). WMC is a leading producer of specialty machinery in the United States. At the end of 2006, WMC purchased York Tool Company (YTC), an Australian firm in a similar line of business. YTC has partially integrated its marketing functions within WMC but still maintains control of its operations and secures its own financing. Following is a summary of the income statement and balance sheet for YTC (in millions of Australian dollars - AUD) for the past three years as well as exchange rate data over the same period.

Smith has discovered that WMC has a small subsidiary in Ukraine. The Subsidiary follows IAS accounting rules and uses FIFO inventory accounting. The Ukrainian subsidiary was acquired ten years ago and has been fully integrated into WMC's operations. WMC obtains funding for the subsidiary whenever the company finds profitable investments within Ukraine or surrounding countries. According to forecasts from economists, the Ukrainian currency is expected to depreciate relative to the U .S . dollar over the next few years. Local currency prices are forecasted to remain stable, however.

One of the managers at WMC asks Smith to analyze a third subsidiary located in India. The manager has explained that real interest rates in India over the last three years have been 2.00%, 2.50%, and 3.00%, respectively, while nominal interest rates have been 34.64%, 29.15%, and 25.66%, respectively. Smith requests more time to analyze the Indian subsidiary.

If WMC uses the temporal method, YTC's net monetary liabilities leave WMC exposed to loss in the event of:

Under che temporal method, the nonmonetary assets and liabilities are remeasured at historical rates. Thus, only the monetary assets and liabilities are exposed to changing exchange rates. Therefore, under the temporal method, exposure is defined as the subsidiary's net monetary asset or net monetary liability position. A firm has net monetary assets if its monetary assets exceed its monetary liabilities. If the monetary liabilities exceed the monetary assets, the firm has a net monetary liability exposure.

Since very few assets are considered to be monetary (mainly cash and receivables), most firms have net monetary liability exposures. If the parent has a net monetary liability exposure when the foreign currency (AUD) is appreciating, the result is a loss. Conversely, a net monetary liability exposure coupled with a depreciating currency will result in a gain. (Study Session 6, LOS 23-c)

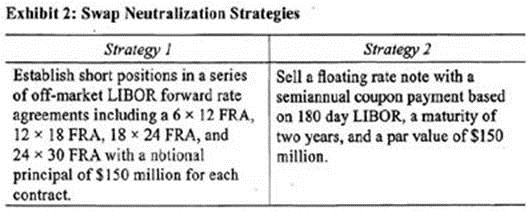

William Bow, CFA, is a risk manager for GlobeCorp, an international conglomerate with operations in the technology, consumer products, and medical devices industries. Exactly one year ago, GlobeCorp, under Bow's advice, entered into a 3-year payer interest rate swap with semiannual floating rate payments based on the London interbank offered rate (LIBOR) and semiannual fixed rate payments based on an annual rate of 2.75%. At the time of initiation, the swap had a value of zero and the notional principal was set equal to $150 million. The counterparty to GlobeCorp's swap is NVS Bank, a commercial bank that also serves as a swap dealer. Exhibit 1 below summarizes the current LIBOR term structure.

Upper management at GlobeCorp feels that the original swap has served its intended purpose but that circumstances have changed and it is now time to offset the firm's exposure to the swap. Because they cannot find a counterparty to an offsetting swap transaction, management has asked Bow to come up with alternative measures to offset the swap exposure. Bow created a report for the management team which outlines several strategies to neutralize the swap exposure. Two of his strategies are included in Exhibit 2.

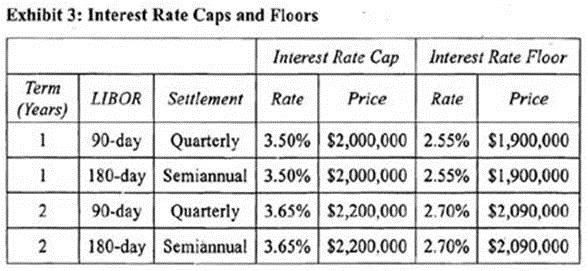

After examining its long-term liabilities, NVS Bank has decided that it currently needs to borrow $100 million over the next two years to finance its operations. For this type of funding need, NVS generally issues quarterly coupon short-term floating rate notes based on 90-day LIBOR. NVS is concerned, however, that interest rates may shift upward and the LIBOR curve may become upward sloping. To manage this risk, NVS is considering utilizing interest rate derivatives. Managers at the bank have collected quotes on over-the-counter interest rate caps and floors from a well known securities dealer. The quotes, which are based on a notional principal of $100 million, are provided in Exhibit 3.

One of the managers at NVS Bank, Lois Green, has expressed her distrust of the securities dealer quoting prices on the caps and floors. In a memo to the CFO, Green suggested that NVS use an alternative but equivalent approach to manage the interest rate risk associated with its two-year funding plan. Following is an excerpt from Green's memo:

"Rather than using a cap or floor, NVS Bank can effectively manage its exposure to interest rates resulting from the 2-year funding requirement by taking long positions in a series of put options on fixed-income instruments with expiration dates that coincide with the payment dates on the floating rate note."

"As a cheaper alternative, NVS can effectively manage its exposure to interest rates resulting from the 2-ycar funding requirement by creating a collar using long positions in a series of call options on interest rates and long positions in a series of call options on fixed income instruments all of which would have expiration dates that coincide with the payment dates on the floating rate note."

Determine which of the interest rate derivatives in Exhibit 3 is appropriate to manage the interest rate risk associated with NVS Bank's $100 million debt obligation and calculate the payoff from this derivative 360 days after the contract initiation if LIBOR at that time is expected to be 3.75%.

NVS Banks is issuing a $100 million floating rate note with quarterly interest rate payments and a maturity of two years to fund its operations. The interest rate risk of such a measure is that interest rates will rise dramatically causing the interest cost on the floating rate note to increase as well. To offset this risk, NVS Bank can take a long position in an interest rate cap. If interest rates rise, the counterparty to the cap will make a payment to NVS Bank. If interest rates fall, no payment is made. Since the cap is a set of interest rate options, NVS has the right to receive payments if the cap is in the money but will never owe any payments if the cap is out of the money. To obtain this option, NVS must pay the cap premium ($2,200,000). The most appropriate cap is the 2-year quarterly payment cap with a contract rate of 3.65%. The expected payoff after 360 days is determined by comparing the expected LIBOR rate (3.75%) to the contract rate on the cap (3.65%). Since the actual rate is expected to be above the cap rate, the cap is in the money and the payoff is calculated as follows:

(Study Session 17, LOS 62.a,b)

Nigel Holmes, CFA, is an investment manager for a small money management firm in London. All of Holmes' clients are citizens of the U.K. Holmes urges all of his clients to maintain internationally diversified portfolios. In his efforts to find undervalued securities, he is currently analyzing a Canadian company called Slapshot, Inc. Slapshot produces hockey equipment at its Canadian manufacturing facilities. About 85% of Slapshot's sales are to the U .S . market, and the remainder are domestic (i.e., in Canada). Sales have been growing at 12% per year. Last year's sales were C$68,000,000. Holmes has gathered the following market information (inflation is perfectly predictable):

* /$ spot exchange rate = 0.8

* /C$ spot exchange rate = 0.4

* U.K. risk-free rate = 6%

* U.K. expected inflation rate = 4%

* Canadian risk-free rate = 9%

* Canadian expected inflation rate = 7%

* U .S . risk-free rate = 4%

* U .S . expected inflation = 2%

Holmes uses the international CAPM (ICAPM) to value international investments. For Slapshot, Holmes believes that the stock's returns are sensitive to the /C$ exchange rate. In order to apply the model, he estimates the following parameters using the as the base currency:

* World market risk premium = 6%

* Sensitivity of Slapshot to the world market = 1.2

* Sensitivity of Slapshot to changes in the /C$ exchange rate = 1.4

* Holmes' expectation for the depreciation of the C$ against the = 2%

* The ratio of the price of the U.K. consumption basket to the Canadian consumption basket is 0.3.

Holmes adds Slapshot stock to several client portfolios at a purchase price of C$ 100. One year later, the stock is trading at C$ 122. There were no dividend payments during the year.

The real /C$ exchange rate is closest to:

The real exchange rate, X, is calculated as follows: S ( / ) S is the spot exchange rate (stated GBP/CAD). Hence, the real exchange rate is 0.4 (1 / 0.3) = 1.33. (Study Session 18, LOS 66.e)

For the past 15 years, Susan Luna, CFA, Kyle Lawson, CFA, and Matt Miller. CFA, have worked together as equity analysts and then equity portfolio managers in the investment management division (BIMCO) of the Broadway Life Insurance Company. For the past five years, the three associates have worked together managing the BIMCO Aggressive Growth Fund (BAGF). During their management tenure the BAGF had excellent performance and was well recognized in the financial press.

Just over one year ago, Broadway Life was acquired by a larger company, Gobble Insurance, and as part of the consolidation process BIMCO was closed. The closure allowed Luna, Lawson and Miller to start their own investment management firm, Trio Investment Management LLC (TIM). TIM focuses on the small capitalization growth equities area. This is the same investment focus as the BAGF, but TIM will have individually managed accounts. Several cases have arisen calling for interpretation as to consistency with CFA Institute Standards of Professional Conduct.

Case 1

TIM markets its investment management services by contracting with small, local bank trust departments. One of the newest bank trust clients for TIM is Shadow Mountain Bank and Trust. Judy Sampson, CFA, the trust officer for Shadow Mountain, has scheduled a meeting with a potential client. When Lawson arrives for the client meeting, he finds that all of the TIM marketing material, including biographies of TIM portfolio managers, has been relabeled by Sampson as the Shadow Mountain Wealth Management Team. Sampson has also added the performance of BAGF into the current TIM Equity Composite Index portfolio and relabeled the resultant combined graph, the Shadow Mountain Equity Composite Index. Sampson states that making such changes would probably please clients and improve the chances of acquiring additional trust management accounts for Shadow Mountain and TIM. Lawson goes along and makes the presentation to the potential client using the Shadow Mountain marketing material and the relabeled BAGF/TIM equity performance record.

Case 2

Susan Luna of TIM is meeting with Sol Wurtzel, an institutional salesman for Turn Byer, a large national brokerage firm. Luna complains that TIM*s technology costs are too high, especially their outside software services costs. TIM currently subscribes to two investment-related software services. The first software vendor is StockCal Software Services (StockCal), which provides valuation and stock charting capabilities TIM uses in their equity research and selection process. The other vendor is Add-Invest Software (Add-Invest), a software program providing account management and performance evaluation reporting which TIM uses in developing monthly reports for all clients. In response to Luna, Wurtzel suggests that Turn Byer has an excellent soft dollar trading desk and would be willing to offer to cover TIM's StockCal and Add-Invest expenses through soft dollar commissions. Luna then reviews TIM's projected commission dollars for the year and decides there are more than enough soft dollars to pay the StockCal, AGF and Add-Invest Software bills combined. Luna believes she can be assured of excellent trade execution from Turn Byer and improved profitability for TIM because of the increased use of soft dollars. Luna then directs that the StockCal and Add-Invest software services be paid for with soft dollar or client brokerage dollars.

Case 3

Sol Wurtzel, the equity salesman for Turn Byer, has referred several clients to TIM over the past year. In fact, Wurtzel referrals currently account for almost 20% of the assets managed by TIM. The principals of TIM decide to reward Wurtzel, either by doubling the commissions paid on trades executed through Turn Byer on Wurtzel's referral accounts, or by paying Wurtzel a cash referral fee for each additional TIM account opened by a Wurtzel referral. The principals agree that any cash referral fee would need to be disclosed to clients in advance.

Case 4

Luna notes that her clients have become increasingly aware of the directed client brokerage / soft dollar commissions issue. At a recent meeting with one of her large pension clients. Service Workers Union Local #1418, the subject of directed commissions came up. Upon learning of the commission dollars available to their account, the Union trustees directed Luna to use their client brokerage of approximately $25,000 to donate to a think lank called the Hoover Study Center of Unions at Samford University. Service Workers trustees believed the Hoover study will increase the public awareness of the benefits unions offer to their members and increase union membership. Luna concurs with the trustee's judgment on increasing union enrollment as a great goal, and follows the client's instructions and makes the $25,000 contribution to the Hoover Study Center. Another client, Rosa Lutz, has asked Luna to credit the soft dollar client brokerage proceeds from her personal retirement accounts to Roswell Academy, to update their computer lab. Luna agrees that a new computer lab for Roswell Academy is greatly needed and she allocates 510,000 of Lutz's commission dollars to Roswell Academy.

Did Luna violate the CFA Institute Standards of Professional Conduct and the CFA Institute Soft Dollar Standards by using soft dollar commissions to pay TIM's software subscription costs to StockCal and/or Add-Invcst?

Standard III (A). Luna has violated the CFA Institute Standards of Professional Conduct - Standard III (A) Duties to Clients - Loyalty, Prudence, and Care. Client brokerage is the property or asset of the client and not TIM. In accordance with CFA Institute Soft Dollar Standards, client brokerage should be used only for research products or services that are directly related to the investment decision making process and not the management costs of the firm. In this case, Luna should disclose to TIM's clients that their brokerage may be used to purchase research. In addition, Luna should seek to ensure that Turn Byer is providing best execution to TIM's clients. StockCal is clearly equity research products/services that aid TIM in the investment decision-making process and not the general operation or management costs of the firm. StockCal may therefore be properly paid for with client brokerage soft dollars and is not a violation of the Standards or Code, or the CFA Institute Soft Dollar Standards. However, Add-Invest Software provides TIM's clients with portfolio accounting and performance measurement services and is not related to the investment decision-making process. Therefore, Luna is misusing clienr resources when she uses client brokerage to purchase Add-lnvest Software. Add-Invest is clearly a business expense of TIM and should rightly be paid for by the firm and not clients. Per the CFA Institute Soft Dollar Standards, the product or service received must provide proper assistance to the investment manager in following through with his investment decision-making responsibilities. (Study Session 1, LOS 2.a and 3a,b,c)

Unlock All Questions for CFA Institute CFA-Level-II Exam

Full Exam Access, Actual Exam Questions, Validated Answers, Anytime Anywhere, No Download Limits, No Practice Limits

Get All 715 Questions & Answers