Trusted Worldwide Questions & Answers

CIMA CIMAPRA19-F02-1 Dumps - Pass F2 Advanced Financial Reporting Exam in First Attempt 2026

The CIMA CIMAPRA19-F02-1 exam, F2 Advanced Financial Reporting, is part of the CIMA Professional Qualification. It is designed for candidates building advanced skills in financial reporting, group accounts, and the interpretation of financial statements. This exam matters because it helps validate your ability to apply reporting standards and analyze financial information in practical business situations. For aspiring finance professionals, it is an important step toward stronger technical competence and career growth.

| # | Exam Topics | Sub-Topics | Approximate Weightage (%) |

|---|---|---|---|

| 1 | Financing Capital Projects | Project appraisal methods, funding options, risk and return assessment | 15% |

| 2 | Financial Reporting Standards | Recognition and measurement, disclosure requirements, standard application | 25% |

| 3 | Group Accounts | Consolidation adjustments, intra-group balances, non-controlling interests | 20% |

| 4 | Integrated reporting | Value creation, strategic reporting, stakeholder-focused disclosures | 10% |

| 5 | Analysing financial statements | Ratio analysis, trend interpretation, performance evaluation | 20% |

| 6 | Revision | Mixed-topic review, exam technique, time management practice | 10% |

The exam tests more than memorization. Candidates must show technical knowledge of reporting standards, the ability to interpret and consolidate financial information, and practical judgment when applying concepts to exam scenarios. It also checks analytical skills, clear working, and the ability to manage time effectively across different question types.

How QA4Exam.com Helps You Pass

QA4Exam.com provides the Exam PDF and Online Practice Test for the CIMA CIMAPRA19-F02-1 exam so you can prepare with actual questions and answers in a focused way. The practice test offers a realistic exam simulation that helps you become familiar with the format, pacing, and pressure of the real assessment. With up-to-date questions and verified answers, you can study with greater confidence and reduce guesswork. The Online Practice Test also helps you improve time management, while the PDF version makes it easy to review key questions anytime. Together, these resources are built to support efficient preparation and help you aim for a first-attempt pass.

Frequently Asked Questions

1. What is the CIMA CIMAPRA19-F02-1 exam?

It is the F2 Advanced Financial Reporting exam in the CIMA Professional Qualification. It focuses on advanced reporting, group accounts, financial statement analysis, and related accounting concepts.

2. Who should take this exam?

This exam is intended for candidates pursuing the CIMA Professional Qualification and for learners who want to strengthen their financial reporting knowledge and practical exam skills.

3. Is the CIMA F2 Advanced Financial Reporting exam difficult?

It can be challenging because it requires both technical understanding and application. Candidates usually need solid practice with reporting standards, consolidation, and analysis to perform well.

4. Can I pass with only braindumps?

Braindumps alone are not a complete preparation method. They are most effective when used with active study, review of concepts, and practice that helps you understand why the answers are correct.

5. Do I need hands-on experience to pass?

Hands-on experience is helpful, but candidates can still prepare effectively through structured study and exam practice. Understanding how to apply concepts in exam-style questions is the key requirement.

6. Are QA4Exam.com dumps enough, or do I need other resources?

QA4Exam.com materials are valuable for exam practice, question familiarity, and answer verification. For best results, many candidates combine them with their study notes and revision of core CIMA topics.

7. Can these resources help me pass on the first attempt?

Yes, they are designed to improve readiness through real exam simulation, updated content, and time management practice. Consistent practice with the Exam PDF and Online Practice Test can support first-attempt success.

8. What format do the QA4Exam.com materials use?

The Exam PDF provides a convenient question-and-answer study format, while the Online Practice Test is built to simulate exam conditions and help you practice under timed settings.

The questions for CIMAPRA19-F02-1 were last updated on Jun 4, 2026.

- Viewing page 1 out of 50 pages.

- Viewing questions 1-5 out of 248 questions

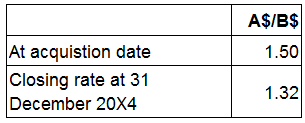

A group presents its financial statements in A$.

The goodwill of its only foreign subsidiary was measured at B$100,000 at acquisition. There have been no impairments to this goodwill.

Exchange rates (where A$/B$ is the number of B$'s to each A$) are as follows:

The value of goodwill to be included in the group's statement of financial position in respect of its foreign subsidiary for the year ended 31 December 20X4 is:

Information from the financial statements of an entity for the year to 31 December 20X5:

The gearing ratio calculated as debt/equity and interest cover are:

ST acquired 75% of the 2 million $1 equity shares of CD on 1 January 20X3, when the retained earnings of CD were S3,550,000. CD has no other reserves.

ST paid $5,600,000 for the shares in CD and the non controlling interest was measured at its fair value of S1,400,000 at acquisition.

At 1 January 20X3, the fair value of CD's net assets were equal to their carrying amount, with the exception of a building. This building had a fair value of $1,000,000 in excess of its carrying amount and a remaining useful life of 25 years on 1 January 20X3.

At 31 December 20X5, the retained earnings of ST and CD were $8,500,000 and $5,250,000 respectively.

What is the value of goodwill to be included in the consolidated statement of financial position of ST as at 31 December 20X5?

VW acquired 240,000 ofthe 300,000 $1 equity shares of EFfor $1,440,000 on 1 January 20X2. Goodwillarising from theacquisition, using the proportionate methodformeasuringnon controlling interest,was $540,000. On 1 January 20X3VW disposed of 30,000of the equityshares in EF for $200,000 cash when thenet assets of EFwere1,200,000. Goodwillarising on the acquisition of EF had not suffered any impairment.

Prepare theaccounting adjustment that will be processed by VW to reflect the disposal of shares in EF when it prepares its consoldiated financial statements.

A group presents its financial statements in A$.

The goodwill of its only foreign subsidiary was measured at B$100,000 at acquisition. There have been no impairments to this goodwill.

Exchange rates (where A$/B$ is the number of B$'s to each A$) are as follows:

The value of goodwill to be included in the group's statement of financial position in respect of its foreign subsidiary for the year ended 31 December 20X4 is:

Unlock All Questions for CIMA CIMAPRA19-F02-1 Exam

Full Exam Access, Actual Exam Questions, Validated Answers, Anytime Anywhere, No Download Limits, No Practice Limits

Get All 248 Questions & Answers